Global Insurance Industry Scenario

With the ever-increasing frequency and severity of natural disasters, Insurers recognize the need to obtain precise information to effectively evaluate and manage potential risks. The increasing sense of urgency has emphasized the requirement for sophisticated, science-driven technological solutions to enhance risk assessment methodologies. It highlights the importance of assessing the potential consequences of such events before assuming risks.

How can NatCat modeling help?

Natural Catastrophe modeling (NatCat) involves using sophisticated statistical and computer models to assess and quantify the potential impact of natural disasters or catastrophes. While natural disasters are inevitable, NatCat Modeling provides a shield against these unknown events. Insurers can use this predictive technology to protect themselves and their policyholders against natural disasters, creating a more resilient future.

NatCat Modeling

- Risk Pricing: NatCat modeling enables quick and repeatable risk assessments for known locations, aiding in calculating robust internal technical prices. The process provides detailed information on hazard exposure, including susceptibility to hazards such as hurricanes or earthquakes, proximity to liquefaction and storm surge risks, and vulnerability assessments based on building standards. Despite inherent uncertainty, benchmark figures facilitate relative risk comparisons over time, enhancing an Underwriter’s decision-making for optimal, long-term pricing.

- Portfolio Management: Similarly, for entire risk portfolios, NatCat modeling efficiently aggregates risk profiles, allowing a direct comparison between diverse assets. For example, serving as a universal benchmark, it enables the evaluation of a high-value industrial facility in Europe against a warehouse in Asia. This strategic use of cat modeling identifies concerns, such as excessive accumulation of correlated risks, and highlights opportunities to enhance the portfolio by adding diversifying risks with minimal impact.

- Capital Requirements: NatCatmodeling’s robust approach to assessing catastrophe risk proves invaluable in determining solvency and meeting regulatory or economic capital requirements. The output from NatCat modeling helps present a complete picture of the exposure risk profile, enabling insurers to integrate these results with other business metrics for informed capital requirement calculations.

OASIS – The Oasis Loss Modelling Framework provides an open-source platform for developing, deploying, and executing catastrophe models. Oasis is an Insurance Industry framework that ensures the results are transparent. (Oasis Loss Modelling Framework | Open source catastrophe modelling platform (oasislmf.org))

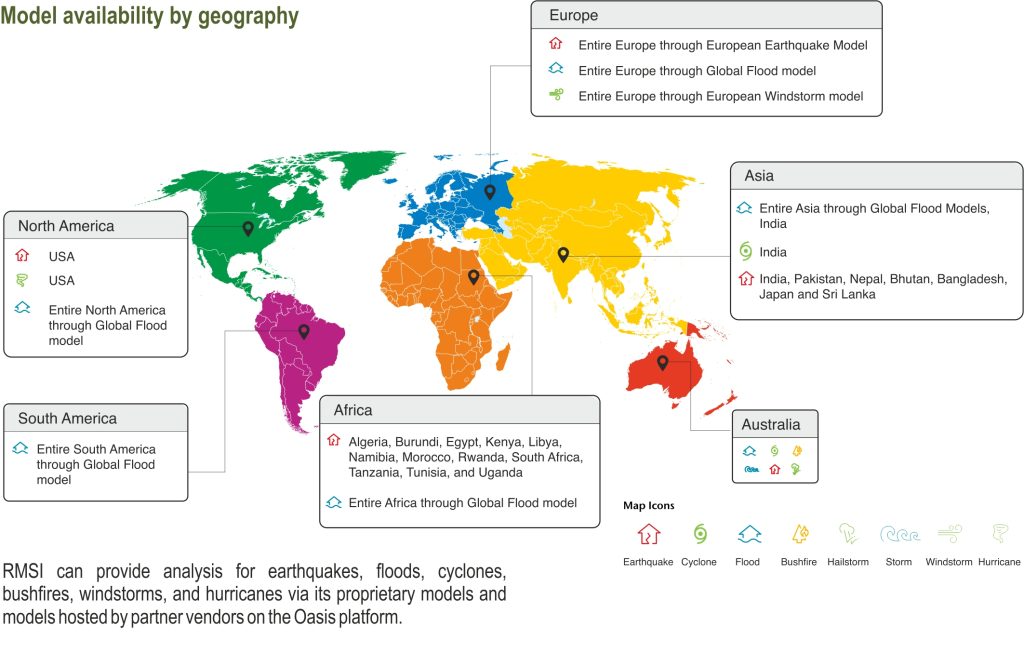

RMSI is an Oasis associate member and provides on-demand global multi-hazard NatCat Risk Analysis through the Nasdaq Risk Modeling for Catastrophes(NRMC) platform (Community Members :: Oasis Loss Modelling Framework (oasislmf.org))

The outcomes obtained following the completion of modeling using the oasis loss modeling framework are:

- EP Curve: Communicates the probability of a given financial loss being exceeded. This approach is used as it is beneficial to identify attachment or exhaustion probabilities, calculate expected losses within a given range, or provide benchmarks for comparisons between risks or over time.

- OEP and an AEP curve: OEP stands for Occurrence Exceedance Probability; AEP stands for Aggregate Exceedance Probability. The OEP represents the probability of seeing any event’s financial impact within a defined period (typically one year) with a particular loss size or greater; the AEP represents the probability of seeing total annual losses of a specific or greater amount.

- VaR and TVaR: VaR stands for Value at Risk; TVaR stands for Tail Value at Risk. Value at Risk is equivalent to the Return Period and measures a single point of a range of potential outcomes corresponding to a given confidence or fixed position. Tail Value at Risk (or Tail Conditional Expectation) measures the mean loss of all possible outcomes with losses greater than a fixed point. These are both mathematical measures used in cat modeling to represent a risk profile, or range of potential outcomes, in a single value.

- Event Loss Table (ELT): ELT is a collection of theoretical Catastrophes (hurricanes, earthquakes, etc.) along with the modeled losses estimated to occur from each event. This forms the raw data used to build up EP Curves and calculate other risk measures.

- Coefficient of Variation (CoV): the standard deviation is divided by the mean (annual average loss). The wider the variation in the distribution of data, the higher the COV.

As catastrophic events continue to rise, stressing the bottom line of reinsurers, the importance of transparent NatCat risk analysis is increasing. RMSI has helped clients by supporting them in facilitating and implementing effective reinsurance strategies by conducting NatCat risk analysis for their exposures. To discuss more, contact us at info@rmsi.com