In this part of my blog, we will talk about the mitigation plan for the climate risks in India. You can find part I of the blog here.

Mitigating the Climate Risks in India

India remained the largest contributor to the growth in emissions in 2022 as it continued to increase its use of coal – the most polluting of fossil fuels (perhaps a short-term measure to cope with the ongoing energy crisis). However, even though India and other countries like China are increasing their emissions quickly, they are still significantly lower per person than in Europe (e.g., Germany burnt more coal in 2022 than in 2021, and the United Kingdom has asked energy firms to delay the closure of end-of-life coal plants). The local climate change is influenced not only by the increase in greenhouse gases but also by the increase in air pollution and the regional changes in land-use patterns (causes can be pretty complex). Facing rapid urbanization and soaring heat, India is now searching for sustainable, clean, and energy-efficient cooling solutions.

| In 2019, the Indian government launched the India Cooling Action Plan, outlining actions needed to provide access to sustainable and energy-efficient cooling. The plan emphasized the importance of passive cooling interventions – the manipulation of architectural elements for cooling such as an eco-friendly response to the issues of sustainable cooling and ventilation to minimize the requirement for Air Conditioners and boost climate resilience and reduce the urban heat island effects. |

Nonetheless, India stands committed to reducing the emissions caused by activities for the nation’s economic growth by 45% by the year 2030 from 2005, according to the updated national targets set by India’s Prime Minister at COP 27 in Egypt. India aims to achieve about 50% of its energy requirements from non-fossil fuel-based energy sources by 2030. The country’s economy will become carbon neutral by 2070 under its longer-term strategies, including the choices listed in the following paragraphs.

A) Switching to Renewable Energy

India is the world’s third largest producer of renewable energy, with 40% of its installed electricity capacity coming from non-fossil fuel sources (although coal still represents the largest share of all energy sources at 73% of total generation while Petroleum and Natural gas are the second major source of energy). The country’s installed renewable power generation capacity has grown rapidly recently, posting a CAGR of 15.92% between FY 2016-2022. As of 31 December 2023, the total installed wind power capacity was 44.736 gigawatts (ranks 4th in global Wind Power capacity with the largest operational onshore wind farm in Kanyakumari district, Tamil Nadu). Renewable electricity is growing faster in India than any other major economy (total installation of solar PV Cells producing 73.32 GW by December 2023), with new capacity additions on track to double by 2026. About 726 square kilometers have been allocated in Rann of Kutch, Gujarat, for the world’s largest hybrid solar-wind power park. The country is also one of the world’s largest producers of modern bioenergy and is ambitious to scale up its use across the economy. To keep its global commitments to source half its energy from non-fossil fuel sources by 2030, India must install about 500 GW of capacity at a considerable investment cost of INR 2.44 lakh crores.

Acquisition of land for installing solar arrays is expensive and must compete with other needs in India. The land required for utility-scale solar power plants is about 1 km2 (250 acres) for every 40–60 MW generated. One alternative is to use the water-surface area on rivers, lakes, reservoirs, farm ponds, and the sea for large solar power plants. The architecture best suited to most of India would be rooftop power-generation systems connected via a local grid, particularly in multi-story housing societies in major urban centers. Also, the outer surface area of tall office complexes and commercial buildings can be used for solar PV power generation by installing PV modules. With multipurpose PV solar plants, India’s floating solar power potential can be enhanced many times by using many inland water bodies. Almost 100 GW of solar power could be generated through a mix of utility-scale and rooftop solar, with the realizable potential for rooftop solar between 57 and 76 GW by 2024.

Nuclear is the safest source of all available electricity generation technologies used to produce electricity globally. Generation III+ nuclear reactors are marketed mainly by China, Russia, and Korea (others include Westinghouse-Sweden). A total of 51 reactors were under construction as of December 2022 (31 of them to be located in China + India + Korea + Russia. Russia is the lead country facilitating the supply and construction of nuclear power projects in foreign countries because it often offers a contract under the ‘build, own, operate’ scheme, and the spent fuel is to be repatriated to Russia, in line with standard Russian practices. India will build two additional nuclear reactors in the coming years under an agreement with Russia.

In India, the unprecedented challenge of climate change in the coming years and decades would require a concerted effort by national government agencies, private businesses, and sub-national climate actions toward rapid acceleration of mitigation efforts across all sectors.

B) Energy Efficiency and Clean Energy Transition in Heat-Intensive Industries

Steel

About 1.9 billion tonnes of steel (one of the most energy-consuming industries) was used globally in manufacturing, from cars to buildings and wind turbines to rockets (at least 12% of the world’s steel goes only in the auto industry) in 2020. By the year 2050, a 30% increase in global steel demand is projected. About 3.7 gigatonnes (Gt) of carbon dioxide (2.6 Gt in direct emissions and 1.1 Gt in indirect emissions) was emitted to the atmosphere in 2020 in making steel (about 9% of the world’s total greenhouse gas emissions). The challenge for the steel sector and the world is to reduce the emissions from steel-making from 3.7 Gt to net zero by 2050 (As against 10 tonnes in the USA, only about 0.4 tonnes of steel is used per capita in India).

Over the past 50 years, technological advances and a move from traditional blast furnaces (BFs) to electric arc furnaces (EAF) have reduced energy use in steel production by 60%. Continued move to EAF will drive down emissions further.

India was the world’s second-largest cement producer (and yet India is the largest importer of cement in the world to meet the growing demand in housing and infrastructure sectors), with production amounting to about 370 million metric tons in 2022 (China’s cement production share equates to over half of the world’s cement and is the biggest cement producer, consumer, and importer in the world). Globally, the cement industry contributes 8 to 9% of GHG emissions, 2 to 3% of its energy demand, and about 9% of its industrial water withdrawals. Cement is considered one of the hard-to-decarbonize industries due to its peculiar energy needs and processes. Cement manufacturing releases CO2 through energy use and calcination reactions. About 8% of India’s total national GHG emissions come from the cement industry, which calls for innovative capabilities to significantly and expeditiously reduce the carbon footprint of this sector. Cement industries in India need to invest in new cement chemistries and other carbon-efficient technologies and repurpose existing manufacturing facilities through measures to consume energy, raw materials, and catalysts.

Hydrogen

A constantly growing number of countries and governments are turning to hydrogen as a possible means of decarbonization and reaching net-zero targets. This opens opportunities in developing countries to create hydrogen development, integration, and adoption strategies. Future clean hydrogen demand will depend on a “Green” climate scenario to reach net-zero emissions by 2050. The demand for hydrogen is expected to rise to 1,300 million metric tons, equivalent to more than twice the energy the world uses today in natural gas (a 160–570% increase from current hydrogen demand). Hydrogen is also crucial in decarbonizing electricity through renewable and battery-based energy storage. The industry with steel and cement sectors is expected to be the second-largest consumer of clean hydrogen. Hydrogen energy can focus on the shipping and aviation sectors in the transport sector. Clean Hydrogen growth will, however, require commitment from countries, manufacturing industries, and business houses.

India plans to use Hydrogen-based (produced with renewable energy) steel production using an EAF that is technically feasible and considered part of a potential long-term solution for decarbonizing the steel industry. Steel manufacturing companies in India must include the impact of carbon emissions when assessing the profitability of capital investments. A better ESG performance can secure project financing at a lower cost, enhance resource management, reduce operational risk, and increase resiliency against future changes.

C) Manufacturing Industries must Strengthen their Pledges to Reduce Carbon Footprints

In recent years, a growing number of commitments and initiatives on advancing climate action with quantifiable targets for reducing GHG emissions, commitments, and pledges are being announced and implemented by companies and investors in cities, states, and regions of India which have a direct impact on national greenhouse gas (GHG) emissions trajectories. Confederation of Indian Industry (in collaboration with WRI – India) analyzed voluntary targets offered by 53 companies in 2014 (which represented 28% of India’s industrial sector emissions) to understand how these relate to India’s national GHG emission projections for 2020 and 2030. This assessment suggests that the voluntary actions by these industries could lead to a 12% reduction by 2030 relative to a business-as-usual scenario. The study also found that almost 50% of the companies were likely to meet their commitments fully.

| Major manufacturing industries such as paper, textiles, jute, sugar, food, petroleum refineries, petrochemicals, and metal/mineral products are responsible for contributing the most greenhouse gases in India. |

These Indian manufacturing industries must make investments in cost-effective actions that can be undertaken to reduce GHG emissions and build resilience that would also increase competitiveness and revitalize the manufacturing sector. With the available technology, resources, and workforce, the private sector must build a clean energy economy and deliver affordable, reliable, clean power to businesses and industries in India.

D) Fuel Switching in India’s Transport Sector

The transportation sector generates the second largest share of greenhouse gas emissions (after energy production), primarily from burning fossil fuel for cars, trucks, ships, trains, and planes. Over 94% of the fuel used for transportation is petroleum-based, including gasoline and diesel. It is also a key contributor to carbon dioxide emissions in India, with energy-related direct emissions at 14% (one of the fastest-growing emission sectors in the country, along with the industrial sector). These emissions have tripled since 1990, with India’s urban population expected to double by 2050 and likely increase further.

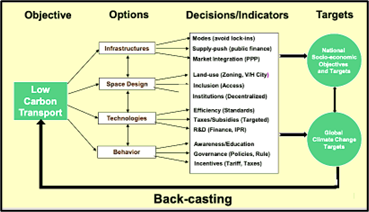

India’s National Action Plan on Climate Change has outlined measures to reduce transport CO2 emissions, including increased public transit, more biofuel use, enhanced vehicle energy efficiency, and other initiatives. India has also developed a roadmap for a ‘Sustainable Low Carbon Transport System’ including technology needs, research and development, technology transfer, finance, and pathways for international cooperation (Figure 4). A long-term (up to 2050) integrated assessment of low-carbon transport transitions (e.g., for infrastructure, vehicle and fuel technologies, etc.) has also been drawn and is under implementation. India unveiled its first indigenous Hydrogen Fuel Cell Bus in Pune last year as the first eco-friendly transportation (the Netherlands, Sweden, Belgium, Luxembourg, and Denmark are the leading countries in green transportation initiatives and infrastructure). Mumbai-based PMV Electric launched India’s first micro-EV late last year to promote sustainable and eco-friendly mobility in the country. These innovations would immensely support India’s aim to be carbon neutral by 2070 as planned.

Methanol is poised to revolutionize energy, powering cars, ships, and homes. It can be produced from various sources, including captured carbon and renewable hydrogen. While conventional fossil fuel methods are established, they have high CO2 emissions. Renewable methanol production is in its early stages, but with supportive policies, it can become cost-competitive and significantly reduce emissions. It will grow significantly if industrial-scale projects will emerge. Notably, India utilizes domestic coal and biomass for methanol production. Viewing methanol as a stepping stone to hydrogen, the government will prioritize investments in its production and infrastructure for swift economic gains in the future hydrogen economy.

E) Mitigating Methane Emissions to Tackle Climate Change in a Shorter Timeframe

Major manufacturing industries such as paper, textiles, jute, sugar, food, petroleum refineries, petrochemicals, and metal/mineral products are responsible for contributing the most greenhouse gases in India. The agriculture, energy, sanitation, and waste sectors are collectively responsible for 90-95% of global anthropogenic sources of methane. The UN has called for a 45% reduction in anthropogenic methane emissions below a 2030 business-as-usual baseline, an aggressive cut that would avoid nearly 0.3°C of global warming by the 2040s while improving human health and agricultural yields through reduced ground-level ozone. U.S., Canada, and Mexico have also pledged to collectively mitigate methane emissions from the oil and gas sector (by fixing leaky pipelines, stopping deliberate releases such as venting unwanted gas from drilling rigs, and other actions in the oil and gas industry), one of the leading sources of human-caused methane emissions. Furthermore, every effort must be made to establish synergies between mitigation options and sustainable development goals(SDGs).

Agriculture accounts for ~41% of methane emissions from human activity, including from rice cultivation and agriculture waste burning, manure management, and gas from cows and sheep; energy accounts for ~35%, including from oil and gas extraction, pumping, transport, and coal mining; and sanitation and waste account for ~20%, including from landfills and wastewater treatment. Humanity generates an estimated 2.24 billion tons of municipal solid waste annually, of which only 55 percent is managed in controlled facilities. The global municipal solid waste could rise from around 2.24 billion tons to 3.88 billion tons by 2050. Every year, around 931 million tons of food is lost or wasted, and up to 14 million tons of plastic waste enters aquatic ecosystems. Food that ends up in landfills generates 8 to 10% of global greenhouse gas emissions. Given the short-term potency of methane, cost-effective interventions to reduce methane emissions should be considered as an immediate priority for the sectors with the largest emissions. While enteric fermentation is the primary source of methane from ruminants, animal manure is also a significant emitter of the gas, as well as of nitrous oxide (constituting 26% of direct emissions; other important sources are synthetic fertilizer and rice cultivation accounting for 13% and 10%). In India, paddy cultivation occurs in a waterlogged environment, favoring methane release. As a result, the rice fields are primarily responsible for the country’s methane emissions.

In a communication to the United Nations Framework Convention on Climate Change, India submitted that approximately 20% of its anthropogenic methane emissions come from agriculture (manure management), coal mines, municipal solid waste disposal, and natural gas and oil systems. According to the Livestock Census of 2020, the total Livestock population in India was 78 million, an increase of 4.6% from the previous census in 2012. As Livestock are also responsible for anthropogenic methane emissions and India accounts for about 30.5% of the world’s cattle inventory, perhaps cutting methane production from Livestock could be vital to climate change mitigation in India. However, the contribution of Indian Livestock to a global pool of enteric methane is meager, as Indian Livestock utilizes large volumes of agricultural by-products and unconventional feed material for cows. Nonetheless, India is the fourth-largest emitter of methane (an increase of almost 30% compared to 1990). Methane emissions come from oil, natural gas, coal, and bioenergy sources.

While reducing carbon dioxide needs to be the long-term focus, it will take a while for us to see the effects of this as carbon dioxide has persisted in the atmosphere for centuries, but cutting down methane emissions can be an excellent short-term target for tackling climate change. Efforts must also go beyond carbon dioxide to include other GHGs, especially short-lived carbon pollutants, like methane (from landfills, agriculture, and the energy industry), which often have a much more intense warming effect despite their shorter life span. Therefore, methane reductions have enormous short-term potential for achieving the temperature goal set in the Paris Agreement.

In the last part of the series, we will discuss the options available with India pertaining to climate risks and the future ahead.