Rural lending has been a neglected area due to traditional lending models, high-cost and low-margin business. But these costs can be reduced by deploying innovative agri-tech solutions to minimize NPAs for banks and agrarian distress for farmers. Let’s explore some details from Saurabh Dayal, Business Development leader at RMSI Cropalytics.

What are the major roadblocks for banks?

The traditional lending models used for offering banking services in urban sections of the country are not entirely suitable for rural areas. Various issues hinder the deployment of banking solutions in rural areas. Firstly, there is a lack of interaction between the lender and borrower. So, there is an absence of reliable data with the banks on the historical credit performance.

Secondly, the ticket size of banking products deployed in rural areas is small, whereas the cost required to service those customers is high. Lastly, the high NPA levels in rural areas are around 3 to 4 times higher than for urban areas. Thus, it becomes less viable to offer solutions.

Apart from the challenges faced by banks, how critical is this situation for farmers?

The farmers encounter difficulties managing their farms as a business, from purchasing inputs to accessing financial services to storing and selling produce. Access to capital has been one of the most significant challenges. Though most banks and financial institutions offer loans to farmers, it is only limited to farmers holding above two hectares of farmland.

Small and marginal farmers, having less than that, go under-banked. But for any farmer, lack of access to finance is not a banking challenge. It’s a livelihood challenge.

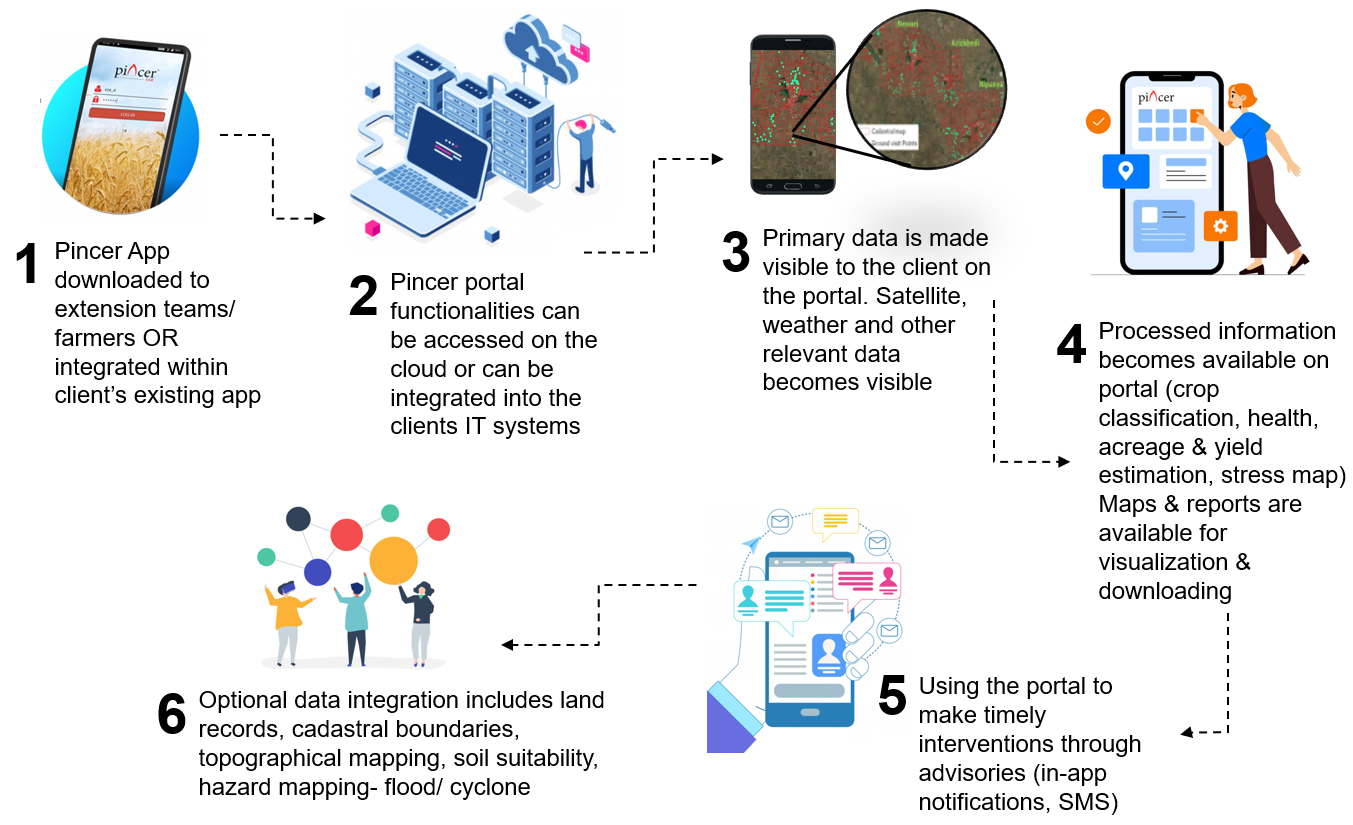

How efficiently can RMSI Cropalytics help banks in addressing agri-lending problems?

How efficiently can RMSI Cropalytics help banks in addressing agri-lending problems?

Inadequate information on villages and farmers before and after the loan disbursal is the prime reason for increasing NPAs. The solution helps banks and lending firms reduce risk by careful debtor selection at the pre-disbursal stage in the priority villages.

Hence, RMSI Cropalytics has developed a complete product suite to cater to different requirements of banks and lending agencies through our Village Prioritization Solution and Farmer Credit Rating solution. These products help understand a village’s profile and determine the farmers’ worthiness in a given village.

Categorizing the risk levels to identify priority villages is one of the critical requirements of banks/lending agencies these days. How well can our solution help in achieving such results?

RMSI Cropalytics Village Prioritization Solution allows clients to evaluate the performance of the villages on a wide array of parameters, including crop type, crop intensity, historical acreages, and yields, along with irrigation, socio-economic and catastrophic scores. The solution enables them to select, choose and modify the model to derive results as required.

This solution helps define how prosperous the villages are or, if I may say, “what is the purchasing power of the village”. The objective here is to categorize villages/farmers in different risk buckets by identifying priority villages for stakeholders. Parameters like crop type, crop intensity, acreages, and crop yields can be used to prioritize villages at the cadastral level as well.

How can banks/lending agencies validate the farmers’ application?

Under the Farmer Credit Rating solution, banks can validate the application with the land record information. We have successfully mapped farmers in over 30% of villages in India, which helps us provide meaningful information to the banks and classify the regional risk bucket in which the applicant falls.

What kind of tech interventions were involved in developing the solutions?

Satellite imagery is deployed to observe different parameters associated with agriculture, such as crop health, cultivation area, cropping pattern, etc., for the past and ongoing season. We also collate data such as farmland area, farmland distance from state and national highway, irrigation source, weather patterns, and other econometric parameters within a particular region for a holistic view.

Also, it verifies whether the farmer or family members have an existing credit history from institutional banks. This fintech solution uses geo-tagging of farmlands for remote monitoring and evaluation. It enables instant credit disbursal in rural areas while reducing operational costs and improves farmers’ portfolio by reducing risks. Financial companies can closely monitor the data points and determine how the farmer does his business or manages risks.

Anything that you would like to add?

The solutions are scalable and can be tweaked as per the banks/lending agencies’ requirements. We can also help them in finalizing their go-to-market strategy and improving ROI by identifying priority areas.

———————————

About RMSI Cropalytics

RMSI Cropalytics is an agri-tech company that combines advanced modeling, machine learning, and agri and meteorological domain expertise to provide detailed information and data analytics on Indian agriculture.

RMSI Cropalytics is a subsidiary of RMSI

Join us at: Twitter | LinkedIn for interesting updates!